Life insurance policies are a critical element of a family’s financial plan. Selecting the right policy ensures your family’s well-being should the unexpected take place.

- Practice Owners

- Employed Physicians

- Practice Managers

- Residents

- Blog

Life insurance policies are a critical element of a family’s financial plan. Selecting the right policy ensures your family’s well-being should the unexpected take place.

Many factors are involved in getting good employees to fill the seats at a medical practice, but job candidates consistently rank group benefits as one of the top factors impacting their decision to accept a job offer. Benefits packages matter; a robust package can make their lives much easier, while a barebones offering forces them to bear most of the monetary or administrative costs themselves.

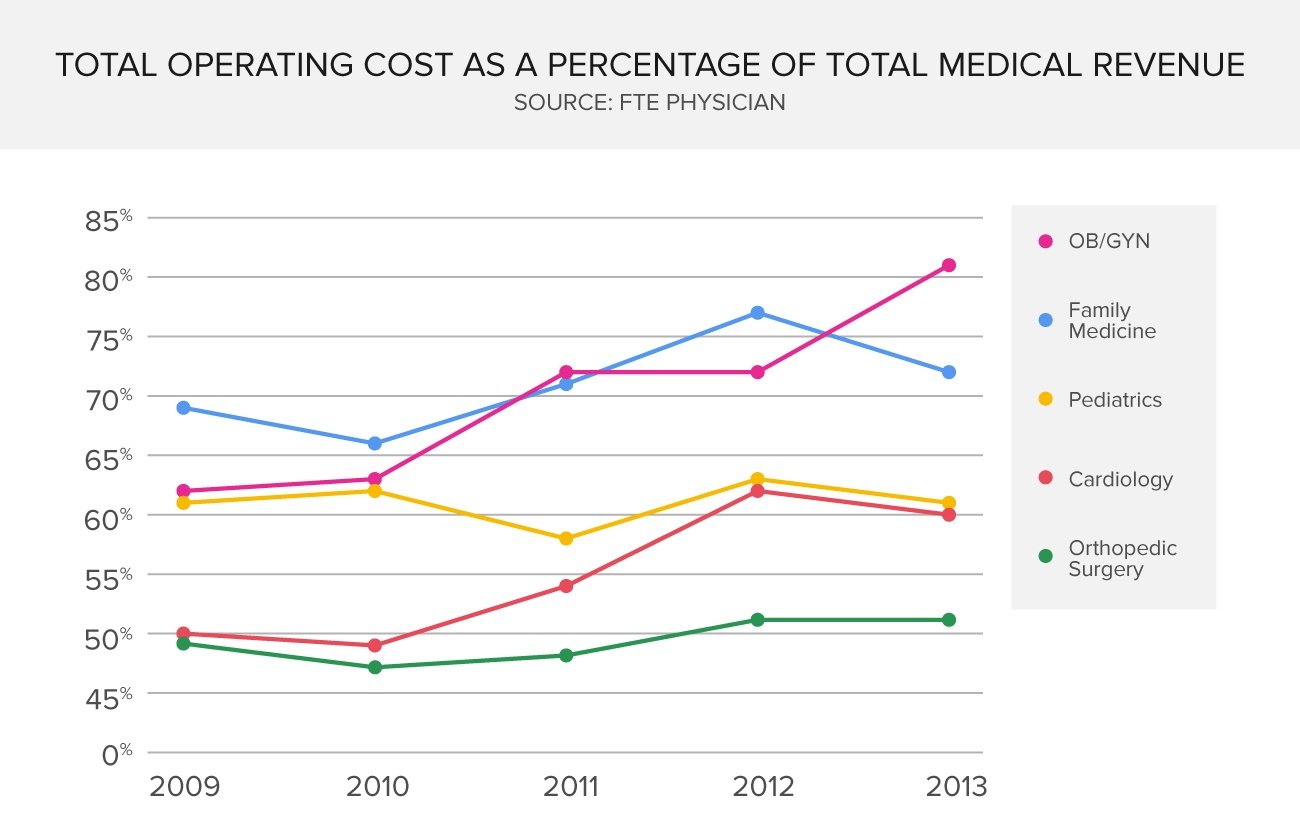

Medical practice owners have a great deal of overhead expenses for which they are responsible. In fact, according to the 2014 MGMA Cost Survey Report, practice operating expenses range from 50% to over 80% of total medical revenue. Additionally, Modern Medicine cited rising operational costs as one of the top 15 challenges facing physicians in 2015. So, what happens to the practice you’ve built if you became disabled?

When you own a successful medical practice there are many people that have helped you grow it. Your amazing team, the ones your practice couldn’t survive without, have had a hand it your success.

According to the National Association of Insurance Commissioners, small businesses are extremely dependent on just a few key people for their success, and 71% say that they are “very dependent” on only one or two key people.

That’s why you should consider purchasing key person life and key person disability insurance for your practice.

Have you ever asked yourself, “Can my business survive if I’m not there”? Most physicians would say no since their practice relies on them so much. Whether you are just starting your own practice, or you are growing an existing one, it’s important that it keeps running smoothly even if something should happen to you.

Like most physicians who own a small or midsize practice, you are the key player in keeping your practice profitable, and if you’re not there to see patients, your practice will quickly fail. Well, that’s what Office Overhead Expense Insurance is there for – a way to keep your business functioning even when you can’t be there.

As you know, a disability can happen to anyone. According to the Council for Disability Awareness, 1 in 4 of today’s 20-year olds will become disabled before they retire. In addition, statistics show that 1 in 8 workers will be disabled for five years or more during their working careers. With statistics like these, it’s pretty hard to turn your back on disability insurance.

The truth is, having a disability will inhibit you from living your life the way you want to and from earning a living. As a physician, you have a high standard of living and you want it to stay that way, which is why you’ve decided to buy disability insurance.

If you are a Texas physician who owns or co-owns a practice, you know there is a lot at stake in addition to your patients’ health. All of the time, energy, money and planning put forth for the practice to be successful should be protected – this is where an Office Overhead Expense Insurance policy comes into play.

An overhead policy can help keep your office running smoothly in the unexpected event that you or another physician becomes disabled and cannot work. Adding up employee’s salaries, utilities, rent, taxes, equipment leases, and other miscellaneous fees, bills begin to mount quickly and can be an added burden upon the practice and the physician while recuperating. Office Overhead Expense Insurance can help keep the doors open and assist you in a variety of ways.

Life insurance – you hear about it often, yet it still seems like a confusing topic. With so many products, solutions and varying opinions, it can be difficult to decide which type of life insurance will best suit your needs and protect your family if the unexpected happens. As a Texas physician, the two main types of life insurance you should familiarize yourself with are Term Life insurance and Permanent Life insurance. Below you will find must-know information regarding both types, in addition to each policy’s pros and cons. Keep this information handy when it comes times to purchase your policy.